Startups in sustainable chemistry and circular economy

There’s a hush in a lab when an experiment finally behaves the way you hoped—relief, disbelief, and a sudden, dizzying clarity of possibility. For founders in sustainable chemistry that hush is the hinge between invention and impact: a molecule that could replace a fossil feedstock, a process that slashes waste, a material that can be returned to the loop. Those moments are intoxicating, but they are fragile. Brilliant ideas too often stall where the real work begins: at scale, in regulation, and in the messy economics of industrial adoption.

Startups in the chemical sector are not just inventing new molecules. They are redesigning value chains to be renewable, circular, and investable. That ambition collides with capital intensity, long development cycles, and industrial risk aversion. The question every founder, investor, and corporate partner asks is the same: where are the real game changers, and how do we accelerate their deployment so that lab breakthroughs become industrial reality.

The valley that separates promise from purchase

Call it the Valley of Death or the commercialization gap. It is the stretch where pilot data meets paying customers, where grant money runs out and project finance is required, where safety, permitting, and supply chains reveal themselves as the true gatekeepers. Many startups with world‑changing chemistry never make it across because they lack the right ecosystem, partners who will host a demo, investors who understand capital intensity, and coaches who can translate lab wins into industrial milestones.

The problem is not a lack of ideas. The problem is a lack of a practical, staged path to deployment. Without that path, the most elegant chemistry remains an academic footnote. With it, a small team in a rented lab can become the supplier that shifts an entire industry toward circularity.

Where the Game Changers surface

The most promising ventures don’t hide in isolation; they surface where deep technical talent meets sector support. When you hunt for a genuine game changer, look for three overlapping signals:

Technical traction: reproducible pilot data, clear process metrics, and a defensible pathway to scale.

Customer engagement: industrial partners willing to host pilots, offtake early volumes, or co‑develop the solution.

Financing runway: a staged capital plan that matches the capital intensity of chemical scale‑up, blending grants, equity, and project finance.

Local acceleration programs, like the Green Chemistry Accelerator, Invest‑NL, and regional development agencies, curate ventures that already show technical promise but need market‑readiness coaching and investor introductions. These programs pair founders with experts and coaches who help shape business plans, set realistic milestones, and secure the partnerships and financing necessary to build pilot plants or enter the market.

Global hubs and multi‑stakeholder platforms

Scaling sustainable chemistry is not a local problem alone; it is a systems problem that requires policy, education, industry, and civil society to move in concert. Multi‑stakeholder centers play a unique role by connecting the dots between research, regulation, and markets. These hubs convene policy makers, public and private sectors, academia, and civil society to align incentives and accelerate adoption.

A center that works across stakeholders does more than fund projects. It shapes policy conversations, builds professional and academic capacity, offers advisory services, and fosters entrepreneurship. By influencing international chemicals policy and training the next generation of practitioners, these centers create the institutional scaffolding that makes industrial pilots replicable and regulatory pathways navigable. When startups plug into these networks they gain more than visibility; they gain legitimacy and a clearer route to scale.

Institutional partners that move the needle

Large, established organizations that commit to bridging the gap between academia and industry are the practical accelerators of scale. Institutions that pledge to focus on the Valley of Death bring three critical assets: technical scale‑up expertise, access to industrial tes-tbeds, and experience spinning research into companies.

Working closely with universities and companies, these organizations advance, apply, and scale research. They collaborate with start‑ups, scale‑ups, and established firms to bring innovations to market because they understand a simple truth: innovation only succeeds if it’s scalable. Their venture arms and spin‑off experience shorten the learning curve for founders by offering operational know‑how, pilot infrastructure, and introductions to strategic partners and investors.

Clues in literature and reports

If you want to find the next wave of game changers, start with the evidence. Studies and reports are beginning to reveal patterns through keyword analysis and mapping exercises that link new technologies to circular economy outcomes. These analyses surface where research clusters, which technologies are converging, and which value chains are most ripe for disruption.

Look for signals such as repeated co‑occurrence of terms like “biorefinery,” “plastic waste,” “digital monitoring,” and “traceability.” Those clusters point to fertile intersections where technical feasibility meets systemic need. Literature reviews and meta‑analyses also highlight which pilot designs answer the right commercial questions and which policy levers most effectively reduce deployment risk.

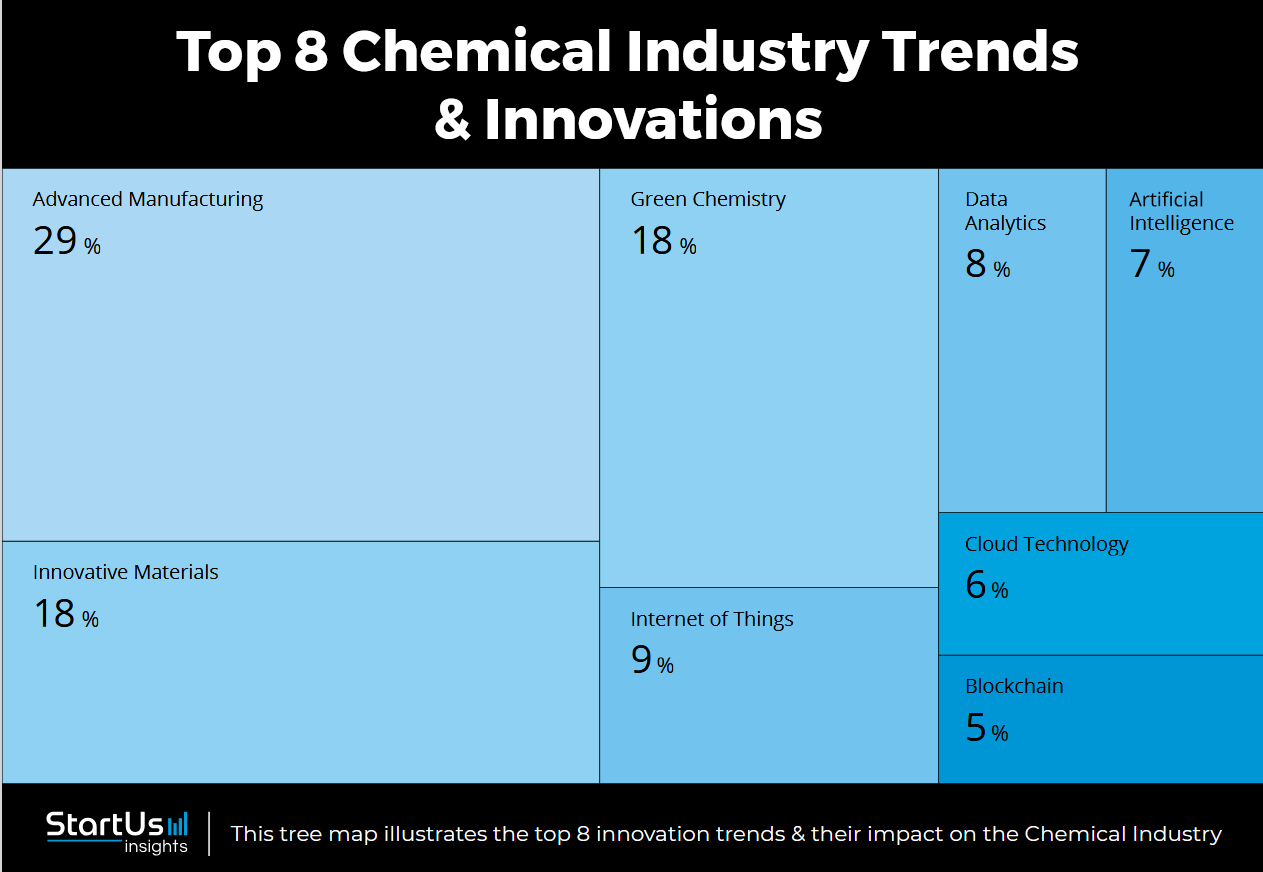

Top 8 chemical industry trends and innovations from the Chemicals Trend report curated by StartUs-Insights

1. Digitalization and AI for operations

What: IoT, AI, cloud, and analytics are optimizing yields, uptime, and safety.

Lesson: Embed sensors and analytics into pilots to produce verifiable KPIs investors trust.

2. Advanced Manufacturing (robotics, AR, digital twins)

What: Digital twins and immersive tools shorten scale‑up risk and training time.

Lesson: Use simulation to de‑risk plant builds and to justify staged financing.

3. Green chemistry and bio‑based feedstocks

What: Shift toward bio‑based alternatives and SSbD (safe‑and‑sustainable‑by‑design) chemicals.

Lesson: Demonstrate lifecycle benefits, not just lab metrics, to capture premium markets.

4. Circularity: recycling, waste‑to‑feedstock, and biorefineries

What: Plastic waste and organic residues are being valorized into chemicals and materials.

Lesson: Design pilots that validate feedstock variability and closed‑loop economics.

5. Innovative materials (biochemistry, nanotech)

What: New polymers, enzyme processes, and nanoscale functionality enable performance parity with petrochemicals.

Lesson: Prioritize manufacturability and end‑of‑life recovery from day one to shorten adoption cycles.

6. Traceability and blockchain for trust

What: Cyber risks and provenance demands make immutable ledgers and material passports essential.

Lesson: Integrate provenance systems into demos so procurement teams can verify circular claims quickly.

7. Security and regulatory alignment

What: Geopolitics, regulation, and cyber vulnerability are reshaping supply‑chain risk.

Lesson: Map regulatory pathways early and include compliance milestones in investor decks.

8. Blended finance and scale‑up ecosystems

What: Grants, equity, and project finance must be staged to match technical milestones.

Lesson: Build a milestone‑linked funding plan and plug into accelerators, research institutions, or corporate testbeds to cross the Valley of Death.

Sustainable chemistry is not a sprint. It is a long, iterative process that rewards patience and ruthless prioritization. Founders must be tenacious enough to iterate through failed pilots and pragmatic enough to pivot when a customer reveals a different problem. Acceleration programs must act as patient capital with operational expertise. Investors must be willing to fund staged de‑risking rather than expect instant returns.

The good news is that the ecosystem is maturing. More accelerators, regional agencies, multi‑stakeholder centers, and established research institutions are aligning to create the pathways that were missing a decade ago. That alignment is what will turn isolated breakthroughs into systemic change.

Bringing startup energy into a century‑old chemical industry works only when rapid iteration is paired with operational discipline: founders must evolve into operators who hire experts, formalize decision rights, and codify a repeatable playbook; pilots need to be designed to expose regulatory, supply chain, and O&M risks and to produce auditable, investor‑grade metrics; and partnerships with industrial hosts, research institutions, and blended finance sources are the fastest route to de‑risking and securing off take, because pace without the right people, systems, and documented evidence simply won’t scale.